This is part 2 in the series. Part 1 on inward remittances is here.

Please note that:

- The focus is on remittances under LRS, mostly for education expenses

- These are retail remittances

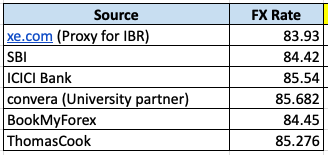

- For comparison, AT the time of writing this blog post, XE showed a rate of Rs 83.92 for $1. This is close to Inter Bank Rate (IBR)

When it comes to paying for international education, outward remittances under the Liberalised Remittance Scheme (LRS) are a key concern for many parents and students. As someone who has been navigating these waters for my daughter’s education, I’ve learned a few things that might help others optimize their remittance process. In this post, I’ll break down the various ways to send money abroad for student fees, focusing primarily on retail transactions, not business-related remittances.

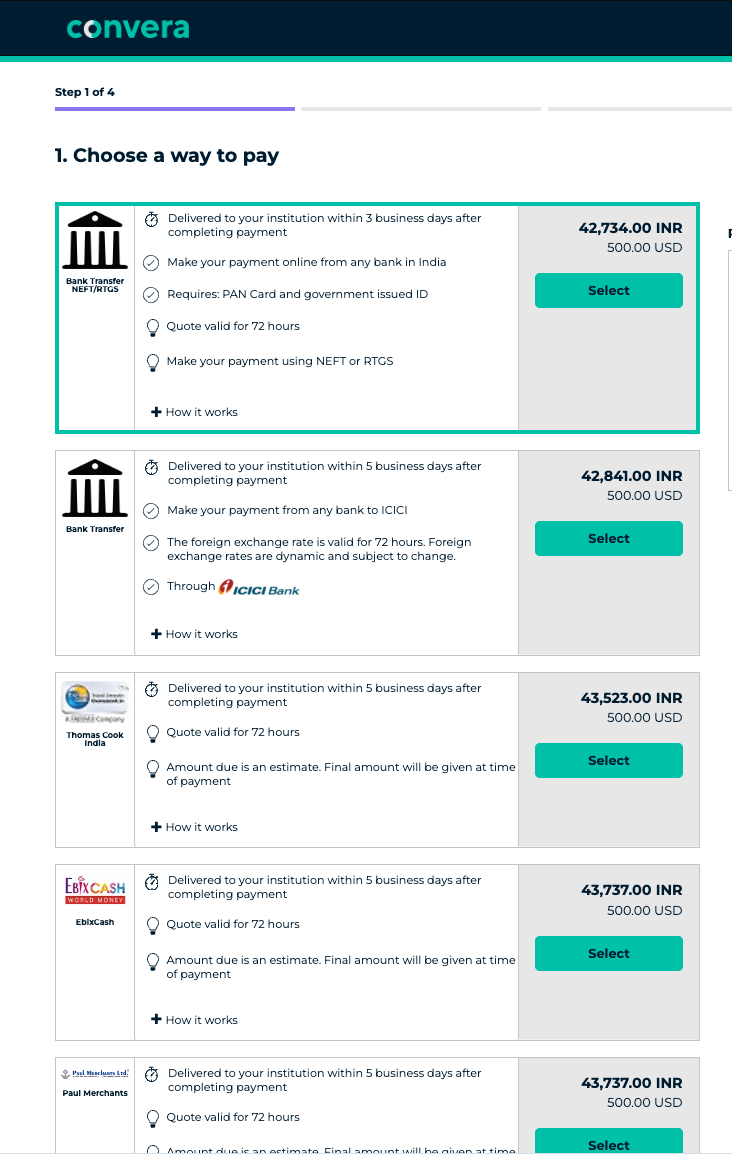

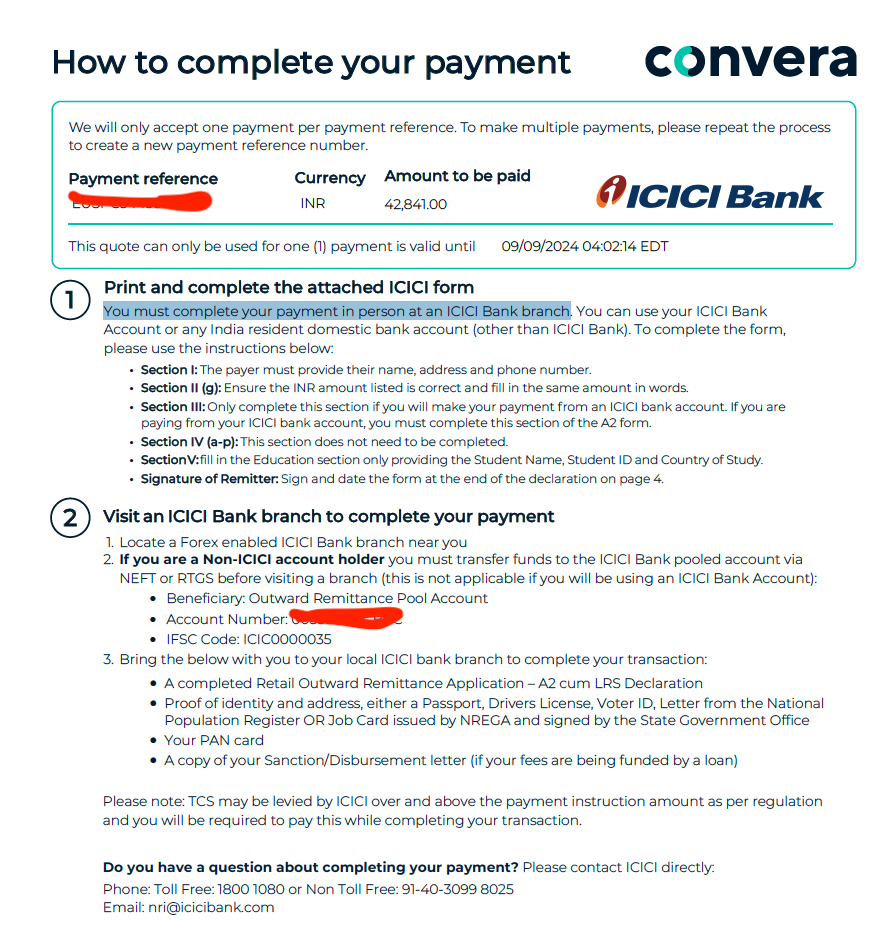

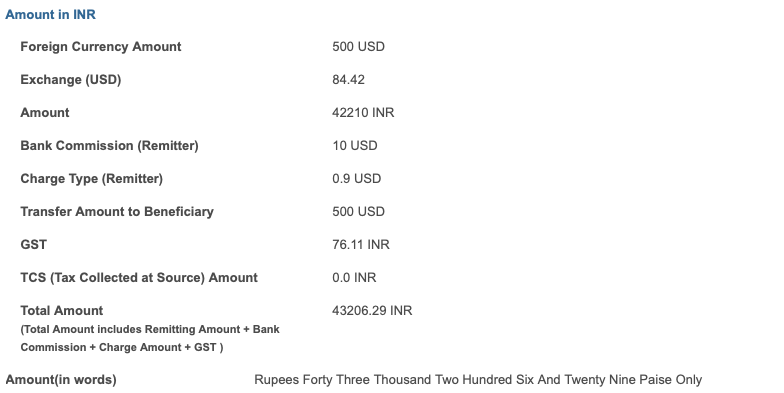

1. Paying Fees via University Partners (Convera and Others)

Most universities partner with financial service providers like Convera to facilitate fee payments. While this might seem like the most convenient option, the exchange rates they offer are notoriously bad. In fact, the FX margins can be much higher than you would get through other channels.

Another downside? The process is not entirely online in most cases. You usually have to fill out a form and physically take it to the bank. This adds to the hassle, especially when you are comparing other, more streamlined methods.

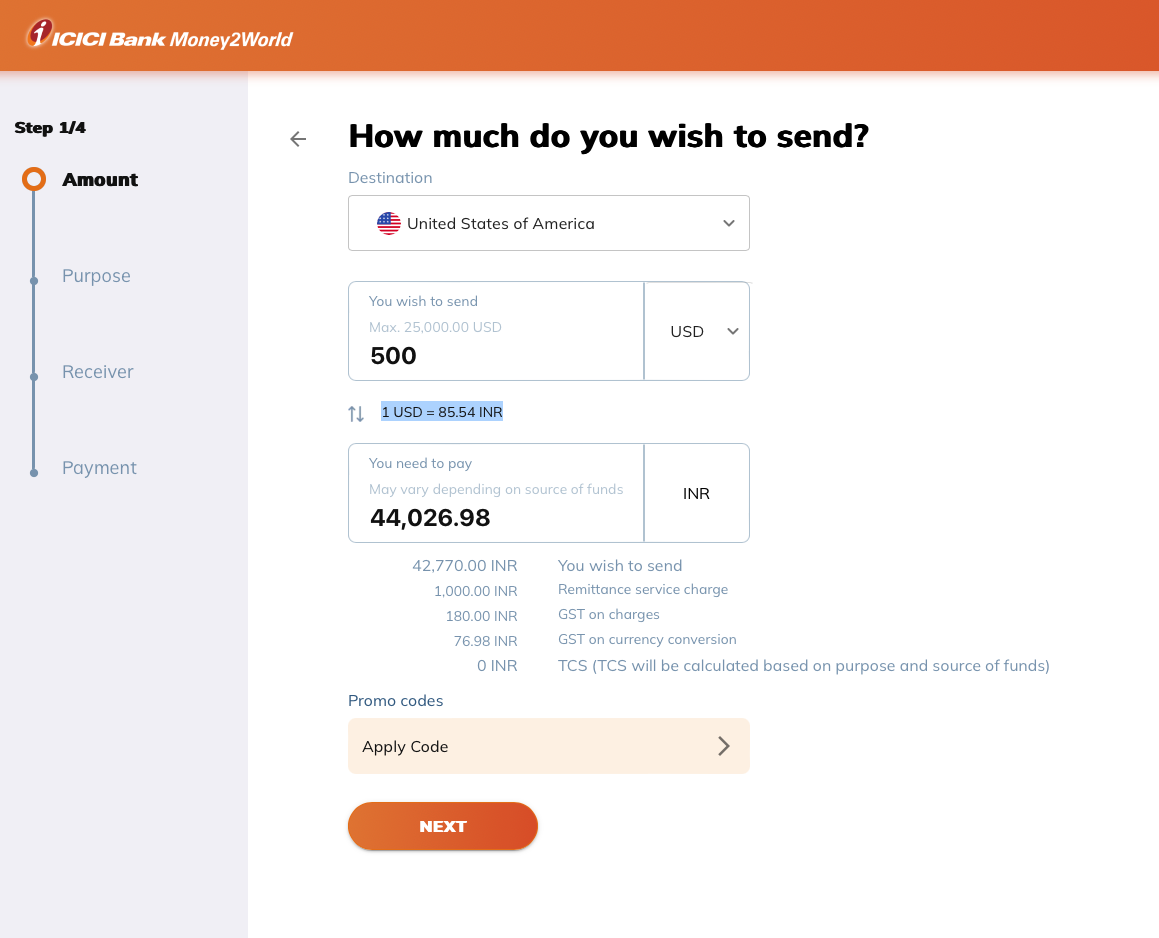

2. Transfer via Your Bank

A more direct way to remit student fees is through your own bank. Request the university to provide their bank account details, and then you can initiate an international SWIFT transfer from your bank account.

Many banks offer the convenience of online transfers, but here’s the catch: the exchange rate can differ greatly depending on how you execute the transfer. This is something you should negotiate with the branch.

- Offline (Branch Transfer): Some banks offer better rates when you go offline. For example, in my case, ICICI Bank charges a 40-50 paise margin over the IBR (Interbank Rate) if I visit a branch and do the transaction in person.

- Online Transfers: However, if you do it online, their FX margin jumps significantly higher, as you can see in the screenshot below. SBI, on the other hand, charges a flat 40 paise margin whether you transfer online or offline, which makes them more consistent.

- FX-Retail Platform: You can also book a deal using RBI’s FX-Retail platform and then provide the deal ID to your bank for the transfer. However, in my experience, this method can be a bit of a headache. The user experience is not ideal, and private banks often don’t offer competitive rates via FX-Retail.

SBI and ICICI exchange rates (online)

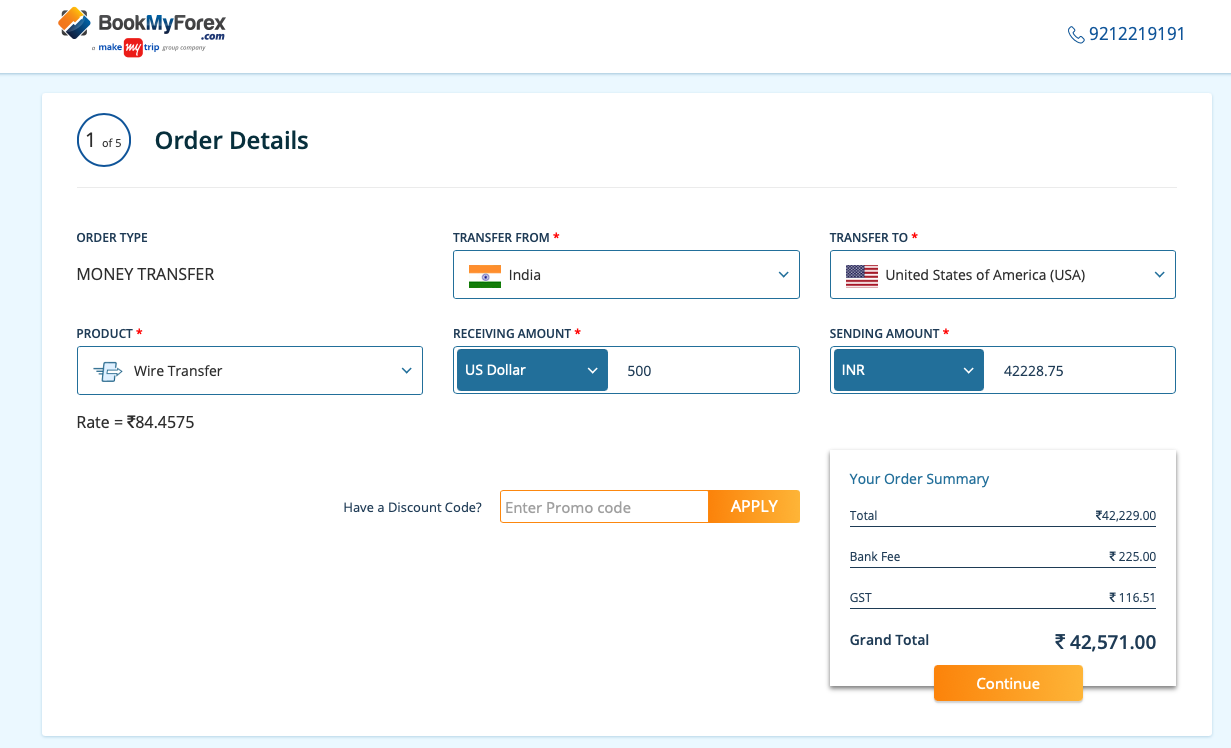

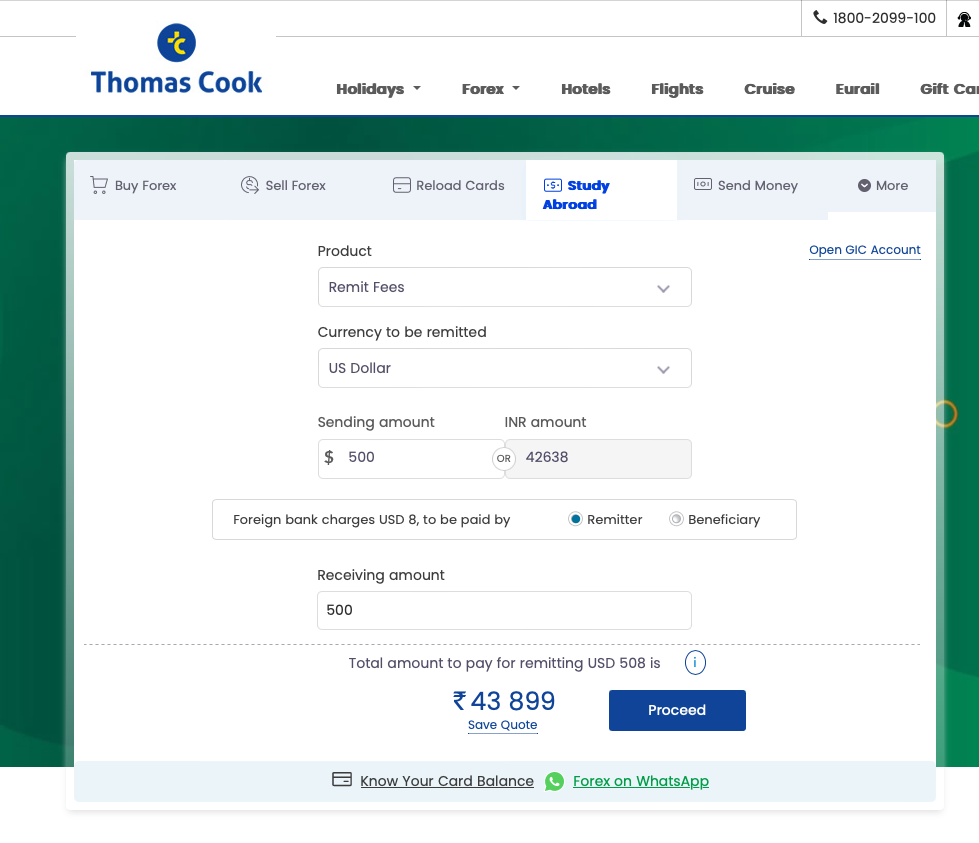

3. Forex Players (Thomas Cook, BookMyForex, etc.)

Several forex service providers, such as Thomas Cook and BookMyForex.com, offer remittance services for student fees. These platforms are often seen as an alternative to banks, but you need to watch out for fluctuating FX margins.

- BookMyForex is currently offering zero FX margins on student fee transfers, making them an attractive option.

- Thomas Cook, however, tends to have high FX margins, which can quickly eat into your remittance amount.

BookMyForex and Thomas Cook exchange rates

While these services change their offers frequently, I personally haven’t found enough incentive to switch from my bank (Option 2) to these services.

4. Other Methods to Consider

Here are a couple of additional methods that might be worth exploring, though they come with their own set of pros and cons:

- International Debit/Credit Cards: Some parents prefer to load an international debit card or credit card with funds and allow their child to pay the fees directly from abroad. While this can work, the FX margin on card transactions is often much higher compared to bank transfers or even forex services. Additionally, there could be foreign transaction fees on top of the FX margin, making this an expensive option for large transfers like tuition fees.

- Remittance Apps (Wise, PayPal, etc.): While Wise (formerly TransferWise) and PayPal are great for sending smaller amounts, they may not be ideal for large transactions like student fees. The reason? High fees and limits on the amount you can send per transaction. They are useful for small, quick payments, but not necessarily for high-value transactions like university tuition.

5. Comparing Costs: Focus on FX Margins, Not Just Fees

For the purposes of this comparison, I’ve primarily focused on FX margins, as this is the most important factor when remitting larger amounts. However, keep in mind that most banks and remittance platforms also levy additional charges such as LRS charges, SWIFT fees, and commissions. These can vary from bank to bank and may include hidden costs that can add up.

For smaller transactions, these charges might seem disproportionately high, so it’s important to keep an eye on them. But for larger transactions like student fees, FX margins are where you should focus your attention, as even a small difference in the exchange rate can translate into thousands of rupees saved or lost.

Conclusion

Here’s a summary of FX rates from all the screenshots above:

Paying student fees abroad under LRS can be done through several avenues, but understanding the hidden costs, exchange rate margins, and processes involved is key to making the most cost-effective decision. While banks provide convenience and better FX margins (especially when done offline), options like BookMyForex offer attractive rates with zero FX margins for now. However, it’s crucial to evaluate all charges and pick the method that suits your individual needs best.

Regardless of the method you use, you can and should always negotiate exchange rates with service providers. For example, most private banks will offer as low as a 10p margin over the IBR even though their card rates are Rs 1.5—Rs 2 over the IBR.

If you’re dealing with remittances yourself and have found other methods that work well, feel free to share them. I’d love to hear what has worked best for others!