Introduction

I see several questions about remittances to and from India. As a professional, I’ve been receiving inward remittances for a very long time. As for outward remittances, I’ve been sending my daughter’s college fees since last year and have been exploring the most cost-effective ways to do so. Therefore, I figured I’ll write what I’ve learned, hoping this will help many others.

This is a two-part series, with inward remittances covered in part 1 and outward remittances in part 2.

For the purpose of this post, Inward remittances are for business income, so they usually go into a current account, whereas outward remittances in this case are LRS (Liberalised Remittance Scheme) remittances from my savings account. Also, my experience has been in USD only but i think this should work for other major currencies too. Keep these disclaimers in mind while reading.

Understanding Inward Remittances for Professionals

For many professionals, inward remittances typically land in a current account. However, using an EEFC (Exchange Earners’ Foreign Currency) account can be advantageous, allowing you to hold the remittance in foreign currency (say USD) and decide when to convert based on favorable exchange rates. The Reserve Bank of India (RBI) permits you to retain the foreign currency until the last day of the next month, giving you flexibility in managing your funds. So if you have EEFC account, you get remittance in foreign currency (say, USD), you park USD in EEFC and then when you convert, the converted INR goes to your current account.

Cost Considerations in Inward Remittances

Understanding the costs associated with inward remittances is essential to maximize your earnings. The main costs include the FX margin and transaction costs (includes conversion cost, intermediary cost, govt GST etc).

- FX Margin: This is the margin over the interbank rate (IBR) that banks or financial institutions apply when converting your USD to INR. For instance, if the IBR is 83 INR/USD, and your bank applies an FX margin of 2%, the rate you receive would be approximately 81.34 INR/USD. This is the most important cost that needs to be reduced.

- Transaction Costs: Some of them, like intermediary costs, correspondent bank costs are outside your control. But others are and can be negotiated.

Option 1: Banks

Most banks publish a card rate for their exchange rates, which is essentially the IBR plus a margin. Typically, this margin can be as high as 2-3%, translating to about Rs 2 per dollar. However, it’s crucial to negotiate with your bank to reduce this margin. For many current accounts, banks may lower the margin to about 5-10 paise over the IBR, significantly reducing your costs.

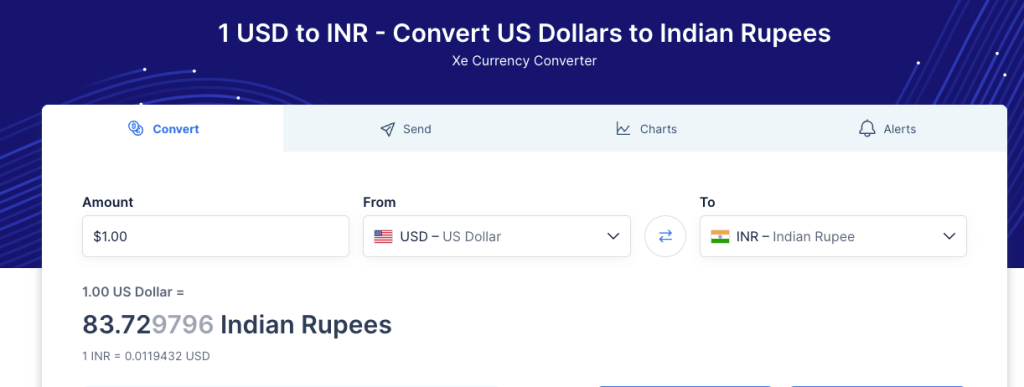

Here’s an example of ICICI Bank’s card rate. Notice that the rate is 81.87 to a dollar. For comparison, i have also attached XE’s rate for comparison. XE rate is closest to IBR. The difference between the two is 83.72-81.87 = Rs 1.85 or more than 2%.

How the Process Works:

- Booking a Deal: You log into your bank’s platform to book a deal, which essentially fixes the exchange rate.

- Providing Deal ID: Once the deal is booked, you provide the deal ID to the bank.

- Conversion: The bank then converts your USD to INR at the booked deal price.

For example, if you book a deal at a 10 paise margin over the IBR of 83, you would get an exchange rate of 82.90 INR/USD. You can also book a deal using RBI’s FX-Retail platform, which allows you to add your banks and book deals directly. However, in my experience, most private banks want you to use their own platforms and may not offer competitive rates via FX-Retail. Public sector banks, on the other hand, are more accommodating with FX-Retail bookings.

Negotiation Tips:

- Emphasize the volume of your transactions as a leverage point.

- Highlight your long-term relationship with the bank.

- Compare offers from different banks to get the best deal.

Transaction costs can vary but may not significantly impact you depending on the volume of your transactions. Nevertheless, it’s worth negotiating these costs as well to further optimize your remittances.

As an example, the screenshot below shows a negotiated rate with ICICI for inward remittances. The rate is 83.625, which is +10p over IBR

Option 2: Online Money Transfer Services

Services like Payoneer, TransferWise (now Wise), and PayPal offer convenient alternatives for inward remittances.

- Process:

- Sign up and verify your account.

- Provide your banking details.

- Receive payments directly into your account.

- Advantages:

- Flexibility to receive proceeds in any of your accounts, not tied to a single bank account.

- Disadvantages:

- Potential limits on transaction amounts.

- High costs

Option 3: Emerging Alternatives

New services like Skydo and xFlow are gaining traction as innovative solutions for inward remittances.

- Pros:

- Competitive rates and lower costs.

- User-friendly platforms.

- Potential for integration with other financial tools.

- Flexibility to receive proceeds in any of your accounts, not tied to a single bank account.

- Cons:

- Limited track record compared to established players.

- Availability might be restricted based on regions.

- Some limitations, e.g., on maximium invoice value

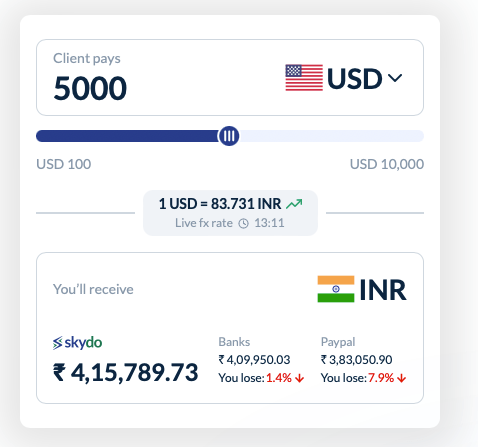

- Cost Considerations:

- Skydo: Zero FX margin but charges a flat fee of $19 for remittances under $2000 or $29 for remittances over $2000.

- xFlow: Charges a 1% FX margin.

Choosing the Right Option

When selecting the best method for inward remittances, consider factors such as speed, cost, convenience, and security. Comparing different options will help you identify the one that best suits your needs. For instance, high-volume transactions might benefit from the lower FX margins negotiated with banks, while occasional transfers could be more cost-effective through online services.

Examples

I have attached screenshots for different options. Below i have summarized the rates so you know the differences. These will help you understand the variations and choose the best option for your needs. All these rates are taken on 30-July-2024, around 1 PM.

| Source | Exchange Rate |

| XE | 83.72 |

| FX-retail | 83.73 |

| ICICI Bank Card rate | 81.87 |

| ICICI Bank Negotiated rate (10p margin) | 83.625 |

| SBI Card Rate | 82.98 |

| Skydo | 83.73 |

Tips for a Smooth Remittance Process

- Double-check all details to avoid errors.

- Time your transfers when exchange rates are favorable.

- Stay informed about potential pitfalls and how to avoid them.

Conclusion

Maximizing your inward remittances involves understanding the various options, negotiating costs, and being proactive in managing your remittances. By choosing the right method and staying informed, you can optimize the value of your international earnings. If you have any questions or need further assistance, feel free to reach out. Happy remitting!

Leave a comment